Disbursement Quota Research

Since 2010, the value of assets held by charities has increased dramatically. For years, some have argued that this increase has been much faster than the increase in charitable spending, particularly among foundations, and that not enough money has been flowing to the charities and communities that need it. This criticism was especially prevalent during the COVID-19 pandemic, when demand for services surged and many organizations struggled to stay afloat.

In response, the federal government introduced new measures increasing the minimum amounts charities with property not directly used in charitable activities must spend on their charitable activities each year (known as the disbursement quota or DQ). The new minimum is set as the equivalent of 3.5% of the first million in non-charitable property and 5% of the amount above $1 million. It took effect for fiscal periods starting on or after January 1, 2023 and the government has committed to reviewing it after five years.

This research bulletin presents our first preliminary analysis of the new disbursement quota, looking at how foundations have responded to the new rules. Although the new measures apply to all charities, we focus on foundations because they were the primary focus of the new policy and are most affected by it. We look at which foundations are affected by the changes, how much disbursements have increased, how patterns of disbursement have changed, and the impact on foundation assets, particularly given current economic conditions.

Want the highlights? Start here. Our one-page summary covers the most important numbers: how many foundations are affected by the new rules, how much disbursements have increased, and what the increase is being used for.

Ready to go deeper? Read the full report. The complete bulletin breaks down the findings by foundation type and size, exploring what's driving the numbers, the impact of recent economic trends and highlighting what we still don't know.

Webinar - A Rising Tide? Early evidence on disbursement quota change. Join us on April 20 at 1 p.m. ET as David Lasby, Principal Researcher at Imagine Canada, walks through our preliminary analysis of the new DQ rules and what the early data tells us.

Together, these resources offer a preliminary picture of where things stand - and what questions still need answering as the government prepares to review the most significant changes to disbursement rules in decades.

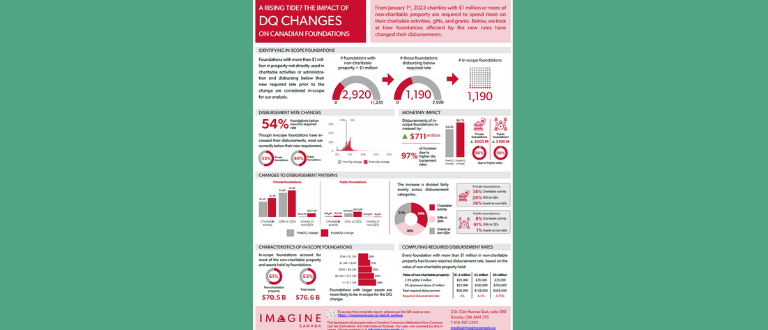

- Foundations are giving more - about $711 million more. That's how much additional money foundations affected by the new DQ disbursed compared to the year before the new rule kicked in. The vast majority of that increase was a direct result of the rule change, rather than an increase in the underlying value of non-charitable property.

- It is taking foundations time to clear the new bar. In the first year under the new rules, 54% of affected foundations underspent their new requirement, meaning they will have to make up ground in following years. Private foundations were slightly more likely to fall short than public ones.

- The timing didn't help. The new requirements landed during a stretch of economic uncertainty and weaker investment returns. Many foundations found themselves being required to give more at a moment when the value of their investments was dropping. This likely explains some - but not all - of the slowness in increasing disbursements.

- Where the money went depended on the type of foundation. Public foundations directed nearly all of their increased disbursements (91%) to other registered charities. Private foundations spread their increases more broadly - across direct charitable work, gifts to qualified donees, and grants to non-qualified donees.

- A headline surplus masks a shortfall. As a group, affected foundations appear to have given $104 million more than required by the quota. But that's because some foundations gave well above the minimum. Strip those out, and disbursements would have been $133 million short.

The government's five-year review of these rules is coming and the stakes are high. Are disbursements higher as a result of the change? Is that increase reaching the communities that need it? And are the rules sustainable over the long term?

This research is a first step in helping build the evidence base needed to support informed decision-making. But it also highlights how much we still don't know. Better data is needed on investment returns, on how charities are managing their assets, and on exactly where donated dollars end up. And the effects of a policy like this take time to play out - one year of data can only tell us so much.

Imagine Canada will continue tracking this issue and sharing findings to support an informed, evidence-based review.

Imagine Canada would like to thank Mastercard Changeworks™ for supporting the production of some of the data used in this report.

Charities with more than $1 million in property not directly used in charitable activities or management and administration are now required to disburse the equivalent of 5% of the average value of that property above the $1 million threshold, up from the old 3.5% requirement.

For example, if a charity has two million in non-charitable property the new rules require it to disburse 3.5% of the first million and 5% of the second million for a total disbursement quota of $85,000 (3.5% of the first million = $35,000 plus 5% of the second million = $50,000 for a total of $85,000). The new requirement took effect for fiscal periods starting on or after January 1, 2023.

The disbursement quota for a given year is based on the average value of non-charitable property over the two years prior to the beginning of the fiscal period being reported. As an example, if a charity measured the value of its non-charitable property on an annual basis and valued that property at $500 in year one and $1,000 in year two, it would report $750 as the value of its non-charitable property in year three (assuming one year fiscal periods).

We focus on foundations for a number of reasons. First, they are much more likely to be affected by the new requirement. Second, they hold a significant majority of the total value of non-charitable property held by charities. Third, because of their role as funders they have very significant impacts on the rest of the charitable ecosystem. Finally, because much of the advocacy around the development of the new rules focused on foundations and they are the major focus of the new rules.

First, we identified the foundations that were affected by the changes. By definition, the changes only apply to foundations with more than $1 million in non-charitable property. Then, among that group, we identified organizations that would be required to increase their disbursements to meet the new rules (i.e., they were below what the new requirements would be just prior to the change). After identifying the foundations affected, we assessed how these in-scope foundations changed their disbursements in the first year of the new requirements.

No, it absolutely does not. Foundations not meeting their DQ in one year can disburse more than they are required to in the next year and then apply it to the shortfall in the first year. For example, if a foundation is $1,000 under the DQ in year one, it can disburse an extra $1,000 above its requirement in year two, apply it to the year one shortfall, and be in compliance.

When introducing the new rules, the government committed to reviewing their impact after five years. We’re doing this analysis to help give all stakeholders a common understanding of what the public T3010 data show about how the new policies are working. As such, our analysis hews as closely as it can to the rules (e.g., accounting for carry-forward of excess disbursements, basing DQ calculations on reported values of line 5900, etc.). To be clear, we are not attempting to evaluate compliance - we’re trying to describe how disbursements are changing in response to the new requirements.

When identifying in-scope foundations we accounted for any over-contributions in the previous five years. It is important to note, however, that when evaluating how disbursements changed with the new rules we looked only at the years immediately before and after the change. We did this for two reasons. First, because we’re trying to see changes over a short period. Second, because it would have penalized foundations for historic shortfalls below the old 3.5% threshold up to five years prior to the rule change.

We focus on non-charitable property because it is the base for the DQ calculation. We can’t be certain exactly why other discussions have focused on other measures, but we do note that historically it used to be fairly common for charities to fail to report their non-charitable property. Having looked at the data over a fairly long period, it is clear that non-charitable property reporting has significantly improved. While we are sure that some property is not being reported, we don’t currently believe it has a major impact on the overall accuracy of our estimates. In our judgement, it is better not to add ambiguity by imputing the value of unreported non-charitable property when assessing short-term change due to the new rules.

There are a couple of things at work here explaining why our estimate is lower.

First, we focus on foundations that we believe were actually affected by the change. Much of the total increase cited above is from foundations that weren’t affected by the change - either they don’t have more than $1 million in non-charitable property or they were already disbursing above the new requirement.

Second, comparing total disbursements without looking at the disbursement rate (the value of disbursements as a percentage of the DQ) conflates the impact of rate changes and the impact of changes in the value of non-charitable property. As an example, if the average value of a foundation’s non-charitable property went from $1 million to $2 million and its disbursements from $35 to $70 thousand, that increase would be entirely due to changes in the underlying value of the non-charitable property (i.e., it would not be because of the rule changes).

Third, because the new policy took effect for fiscal periods starting on or after January 1, 2023 about three fifths of 2023 foundation T3010 returns were actually their first returns after the rules changed. The vast majority of foundations filing for a December 31, 2023 year end had a fiscal year beginning on January 1, 2023 and were subject to the new rules. Unless they were filing returns adjusting their fiscal period (which would be shorter than a year), which very, very few did, foundations filing 2023 returns for year ends earlier than December 31st were not subject to the new rules.

Yes it does. As part of our analysis we assess the role of grants to NQDs, compared to other forms of qualifying disbursements. We intend to look at the issue in greater detail in a forthcoming Research Bulletin.